📊 Executive Summary & Investment Thesis

National Securities Depository Limited (NSDL) stands ready to make its highly anticipated market debut with an IPO expected to open on July 30, 2025, and close on August 1, 2025. As India’s largest and oldest depository, NSDL represents a unique investment opportunity in the backbone infrastructure of India’s rapidly growing capital markets.

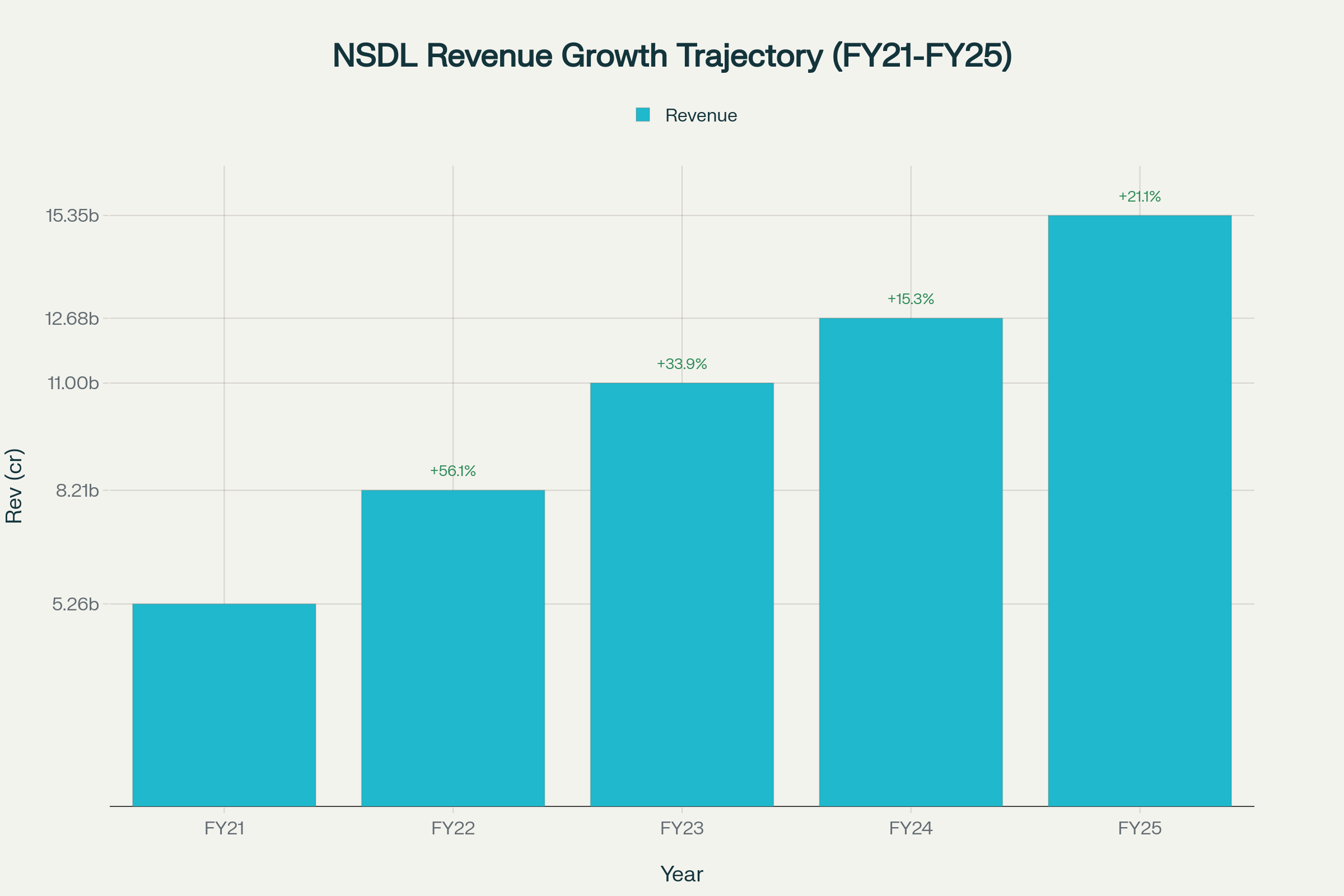

NSDL Revenue Growth Trajectory showing consistent growth from ₹526 crores in FY21 to ₹1,535 crores in FY25

The company is targeting an Offer for Sale (OFS) of approximately ₹3,000-3,400 crores through the sale of 5.01 crore equity shares by existing shareholders including IDBI Bank, NSE, SBI, and HDFC Bank. With an expected price band of ₹750-800 per share, the IPO values NSDL at ₹15,000-16,000 crores.

💼 IPO Details & Key Information

| Parameter | Details |

|---|---|

| Opening Date | July 30, 2025 |

| Closing Date | August 1, 2025 |

| Expected Price Band | ₹760-800 |

| Issue Size | ₹3,000-3,400 Crores |

| Face Value | ₹2 per share |

| Issue Type | Complete Offer for Sale (OFS) |

| Grey Market Premium | ₹166 |

| Expected Listing | BSE & NSE |

| Market Cap | ₹15,000-16,000 Crores |

🎯 Key Selling Shareholders

- IDBI Bank (26.01% stake) – Major seller

- National Stock Exchange (NSE) (24% stake) – Primary seller

- Union Bank of India – Reduced offer to 5 lakh shares

- State Bank of India (SBI) – Participating in OFS

- HDFC Bank (8.95% stake) – Halved original offer size

📈 Fundamental Analysis: Strong Financial Performance

5-Year Financial Trajectory

| Year | Revenue (₹ Cr) | Net Profit (₹ Cr) | EPS (₹) | ROE (%) | EBITDA Margin (%) |

|---|---|---|---|---|---|

| FY21 | 526.12 | 188.57 | 9.43 | 18.5% | 50.3% |

| FY22 | 821.29 | 212.59 | 10.63 | 17.8% | 36.4% |

| FY23 | 1,099.81 | 234.81 | 11.74 | 16.4% | 29.9% |

| FY24 | 1,268.24 | 275.44 | 13.77 | 17.1% | 22.5% |

| FY25 | 1,535.18 | 343.12 | 17.16 | 17.1% | 24.4% |

Revenue Growth: NSDL has demonstrated exceptional growth with revenue increasing from ₹526 crores in FY21 to ₹1,535 crores in FY25, representing a CAGR of ~30%. The company’s net profit surged 24.57% in FY25 to ₹343 crores.

Profitability Metrics: The company maintains healthy margins with PAT margin of 22.3% in FY25 and ROE of 17.1%. Despite some margin compression due to increased competition and investments, NSDL shows recovery in FY25.

🔍 Technical Analysis & Market Positioning

Peer Comparison & Valuation

Market share comparison between NSDL and CDSL showing NSDL’s dominance in value while CDSL leads in volume

| Metric | NSDL | CDSL | Analysis |

|---|---|---|---|

| Revenue FY25 (₹ Cr) | 1,535 | 1,199 | NSDL leads by 28% |

| Net Profit FY25 (₹ Cr) | 343 | 526 | CDSL higher profitability |

| ROE (%) | 17.1% | 29.2% | CDSL more efficient |

| P/E Ratio | ~50-55x | 67.4x | NSDL valued lower |

| Market Focus | Institutional | Retail | Different strategies |

Market Share Analysis:

- By Value: NSDL dominates with 60% market share vs CDSL’s 40%

- By Volume: CDSL leads with 76% vs NSDL’s 24%

- Strategy: NSDL focuses on high-value institutional clients while CDSL targets retail volume

🏢 Company Profile & Business Model

Core Business Operations

NSDL operates as India’s premier depository, providing critical market infrastructure services

Primary Revenue Streams:

- Issuer Charges – Annual custody fees from securities issuers

- Transaction Fees – Volume-based settlement charges

- Account Maintenance – Fees from depository participants

- e-Governance Services – PAN, KYC, and digital services through subsidiaries

- Value-Added Services – e-voting, pledge services, corporate actions

Market Dominance Metrics

- Demat Accounts: 3.88 crore (institutional-focused)

- Registered Issuers: 64,535 (double of CDSL)

- DP Service Centres: 63,542 locations

- Average Asset Value per Account: ₹1.25 crore (vs CDSL’s ₹5 lakh)

- Assets Under Custody: ₹506.11 lakh crores (US$ 6.04 trillion)

👥 Management & Leadership Analysis

Board of Directors & Executive Team

Current Leadership:

- MD & CEO: Vijay Chandok (Recently appointed November 2024)

- Chairman: Parveen Kumar Gupta (Public Interest Director)

- CFO: Vaishali Vaidya (Interim)

Management Qualifications:

Vijay Chandok brings over 30+ years of BFSI experience, previously serving as MD & CEO of ICICI Securities and executive director at ICICI Bank. The board comprises seasoned professionals from banking, technology, and regulatory backgrounds ensuring strong governance.

🏭 Industry Analysis & Market Dynamics

Depository Services Industry Overview

The Indian depository industry is a regulated duopoly between NSDL and CDSL with high barriers to entry. The sector benefits from:

Growth Drivers:

- Financialization of Savings: Shift from physical to digital assets

- Rising Demat Accounts: 19.24 crore total accounts as of March 2025

- IPO Boom: Record IPO activity driving new account openings

- Regulatory Support: SEBI’s push for dematerialization

Market Size & Growth:

- Industry Revenue: ₹10.3 billion in FY23 with 20% CAGR (FY18-FY23)

- Projected Growth: 10-11% CAGR to reach ₹15-15.5 billion by FY27

- Total Market Cap: ₹78,028 crores for listed depository services companies

📊 Quantitative Analysis & Valuation Metrics

Balance Sheet Strength

| Metric | FY25 | Analysis |

|---|---|---|

| Total Assets | ₹2,093 crores | Strong asset base |

| Book Value/Share | ₹100.27 | Solid backing |

| Debt-to-Equity | 0.00 | Debt-free operations |

| Current Ratio | Strong | Excellent liquidity |

| Cash & Equivalents | ₹145 crores | Healthy reserves |

Cash Flow Analysis

- Operating Cash Flow FY25: ₹558 crores (strong conversion)

- Investing Activities: Heavy investments in technology and growth

- Free Cash Flow: Consistently positive with reinvestment focus

🎯 SWOT Analysis

Strengths 💪

- Market Leadership: India’s largest depository by value and institutional presence

- Regulatory Moat: High barriers to entry in regulated duopoly

- Diversified Revenue: Multiple income streams reduce cyclical risks

- Technology Infrastructure: State-of-the-art systems and security

- Government Backing: Strong institutional shareholder base

- Financial Health: Debt-free with consistent profitability

Weaknesses ⚠️

- Retail Penetration: Lower retail account base compared to CDSL

- Volume Market Share: Only 24% market share by transaction volume

- Margin Pressure: Competition affecting profitability margins

- Regulatory Dependency: Subject to SEBI regulations and policy changes

- Limited Growth Avenues: Mature core business requiring diversification

Opportunities 🚀

- Digital Transformation: Expanding e-governance and fintech services

- Market Expansion: Growing retail investor base in India

- New Asset Classes: Bonds, insurance, pension products dematerialization

- International Expansion: NRI services and global partnerships

- Technology Services: Monetizing IT infrastructure for third parties

- ESG Services: Growing demand for sustainability reporting

Threats 🛡️

- Intense Competition: CDSL’s aggressive retail market capture

- Regulatory Changes: Policy shifts affecting business model

- Technology Disruption: Blockchain and new technologies

- Economic Slowdown: Market volatility affecting transaction volumes

- Cyber Security: Rising digital threats requiring constant upgrades

🌍 Macro & Micro Economic Factors

Macroeconomic Tailwinds

- GDP Growth: India’s 7%+ GDP growth supporting capital market expansion

- Financial Inclusion: Government’s push for digital financial services

- Demographic Dividend: Young population driving investment activity

- Digital India: Massive digitization creating opportunities for NSDL’s e-gov services

Microeconomic Factors

- Rising Disposable Income: Increasing retail investor participation

- Corporate Growth: More companies accessing capital markets

- Mutual Fund Growth: SIP culture driving regular investment flows

- Regulatory Support: SEBI’s initiatives promoting market development

🏆 Competitive Analysis & Market Position

Versus CDSL (Primary Competitor)

NSDL’s Competitive Advantages:

- Institutional Dominance: Preferred by large corporations and FIIs

- Higher Asset Quality: ₹1.25 crore average per account vs CDSL’s ₹5 lakh

- Infrastructure Depth: More service centers and broader reach

- Government Projects: Strong presence in e-governance through subsidiaries

CDSL’s Competitive Edges:

- Retail Volume Leadership: 76% market share by transaction volume

- Higher Profitability: Better margins and ROE

- Agile Technology: Faster onboarding and modern systems

- Growth Momentum: Benefiting from retail investor surge

🏢 Subsidiary Analysis & Corporate Structure

Key Subsidiaries

- NSDL Database Management Limited (NDML)

- Business: e-KYC, PAN verification, GST services

- Employees: 200+ professionals

- Revenue Contribution: Significant e-governance projects

- NSDL Payments Bank Limited

- Business: Digital banking and financial services

- Employees: 51-200 people

- License: RBI-approved payments bank since 2017

- Services: UPI, digital banking, money transfer

Total Group Strength: 1,000+ employees across the organization with specialized expertise in technology, compliance, and financial services.

💹 Broker Recommendations & Market Sentiment

Analyst Views

Based on market reports and broker analysis:

Positive Factors:

- Quality Business: Monopolistic characteristics with regulatory protection

- Stable Revenue: Recurring income model with defensive characteristics

- Market Infrastructure: Critical role in India’s capital market ecosystem

- Conservative Valuation: IPO pricing appears reasonable versus peers

Concerns:

- Growth Constraints: Mature business model with limited expansion scope

- Competition: CDSL’s aggressive retail market strategy

- Valuation: Premium pricing versus historical metrics

📊 Investment Recommendation & Price Targets

Valuation Analysis

At expected IPO price of ₹750-800:

- P/E Ratio: 44-46x (vs CDSL’s 67x)

- P/B Ratio: 7.5-8.0x

- Enterprise Value: ₹15,000-16,000 crores

- Dividend Yield: ~0.1%

Price Projections

- Conservative Target: ₹850-900 (12-month)

- Optimistic Target: ₹1,000-1,100 (24-month)

- Risk Scenario: ₹650-700 (market correction)

⚡ Key Investment Risks & Mitigations

Primary Risks

- Regulatory Risk: Changes in SEBI policies affecting business model

- Competition Risk: CDSL’s continued market share gains

- Technology Risk: Disruption from blockchain or new technologies

- Market Risk: Economic slowdown affecting transaction volumes

- Valuation Risk: Premium pricing limiting upside potential

Risk Mitigation Strategies

- Diversification: Expanding into e-governance and fintech services

- Technology Investment: Continuous IT infrastructure upgrades

- Strategic Partnerships: Collaborations for market expansion

- Operational Efficiency: Cost optimization initiatives

📋 Final Investment Verdict

NSDL IPO presents a solid investment opportunity for investors seeking exposure to India’s capital market infrastructure with the following characteristics:

✅ Suitable For:

- Long-term Investors: Seeking stable, dividend-paying infrastructure stocks

- Defensive Portfolio: Low-volatility addition to equity portfolios

- Institutional Exposure: Indirect play on India’s economic growth

- Quality Seekers: Strong governance and regulatory compliance

❌ Not Suitable For:

- Growth Investors: Limited high-growth potential

- Short-term Traders: Defensive stock with modest volatility

- Value Hunters: Premium valuation versus historical metrics

Overall Rating: 3.5/5 ⭐⭐⭐⭐

Investment Thesis: NSDL offers a unique opportunity to invest in the plumbing of India’s capital markets. While growth may be moderate, the company provides defensive characteristics, regulatory protection, and consistent cash generation. The IPO pricing appears reasonable, making it suitable for conservative equity allocation with 3-5 year investment horizon.

This comprehensive analysis is based on publicly available information as of July 2025. Investors should conduct their own due diligence and consult financial advisors before making investment decisions. Past performance does not guarantee future results.