Introduction

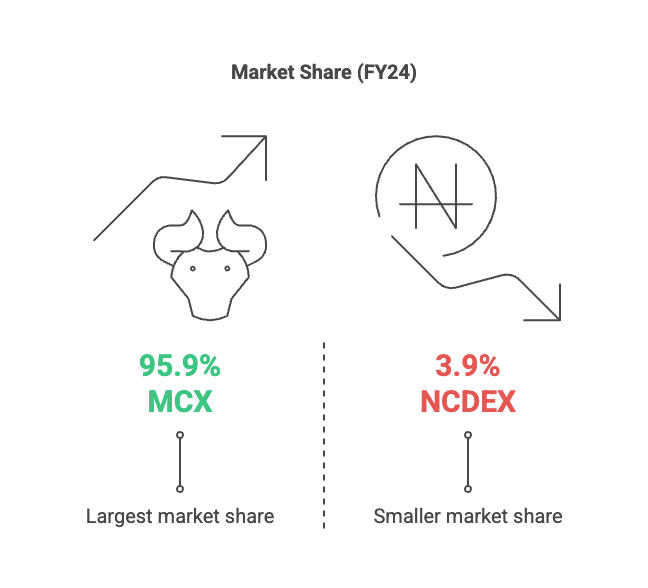

Multi Commodity Exchange of India Limited (MCX), established in 2003, is India’s premier commodity derivatives exchange, facilitating online trading of commodities such as bullion, industrial metals, energy, and agricultural products. Operating under the Securities and Exchange Board of India (SEBI), MCX holds a 95.9% market share in commodity futures (FY24) and is listed on both BSE and NSE (MCX India). This report evaluates MCX’s investment potential in 2025, focusing on its financial health, market position, and growth prospects.

Fundamental Analysis

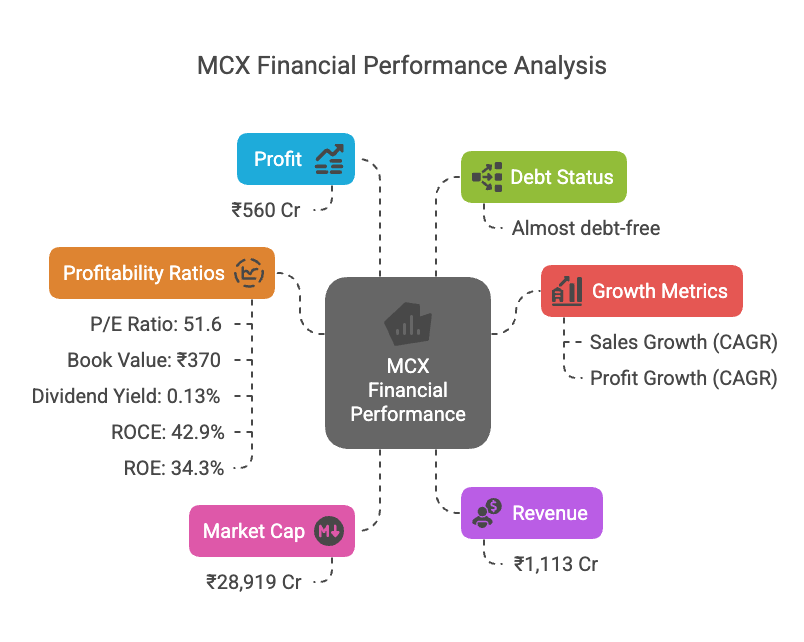

Fundamental analysis assesses MCX’s financial performance, profitability, and growth metrics to determine its intrinsic value. The following table summarizes key financial data for FY25:

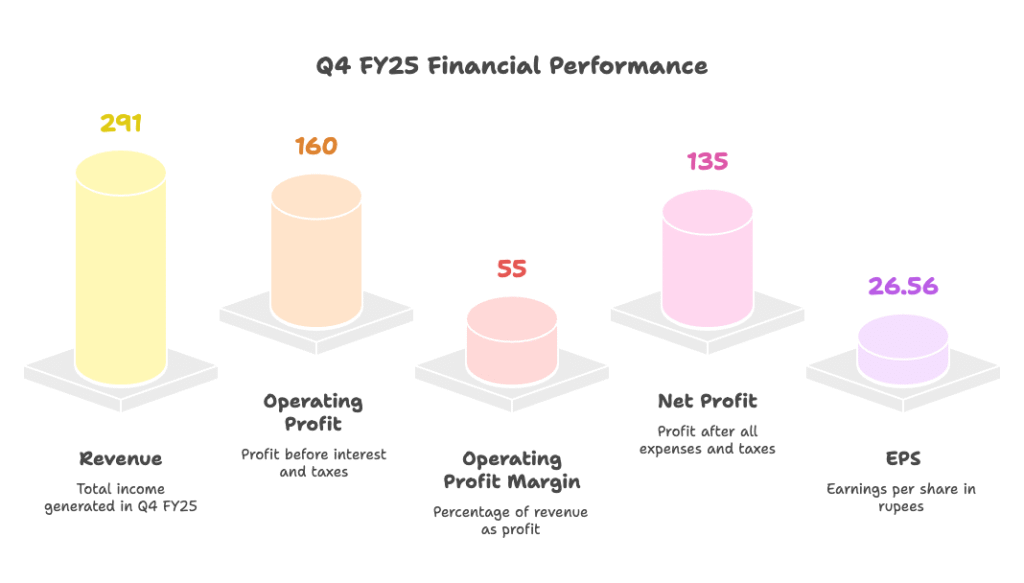

Quarterly Results (Q4 FY25)

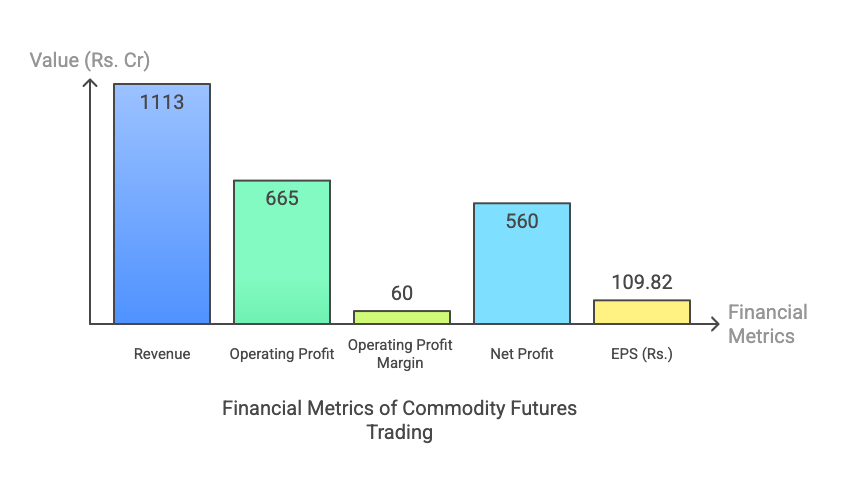

Annual Results (FY25)

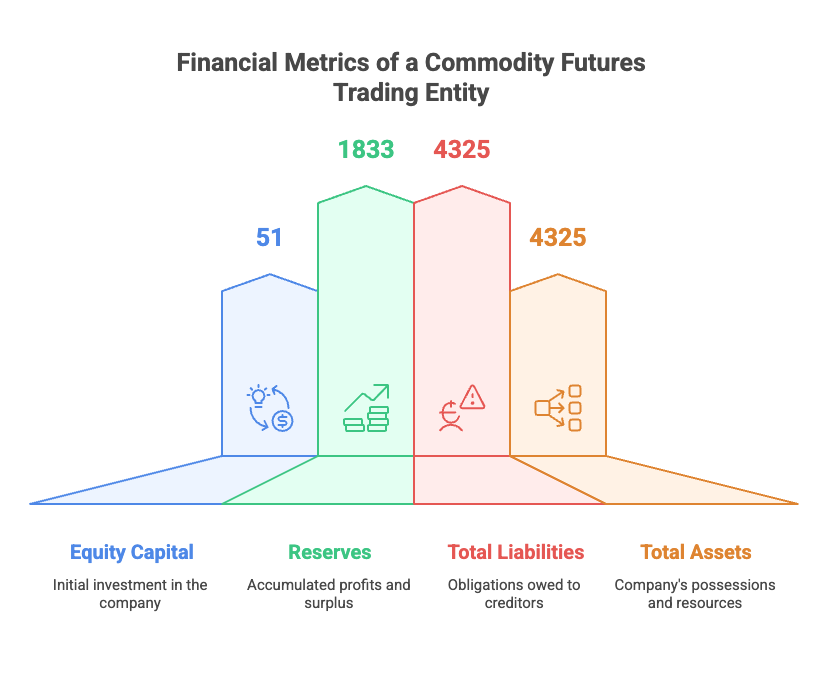

Balance Sheet (Mar 2025)

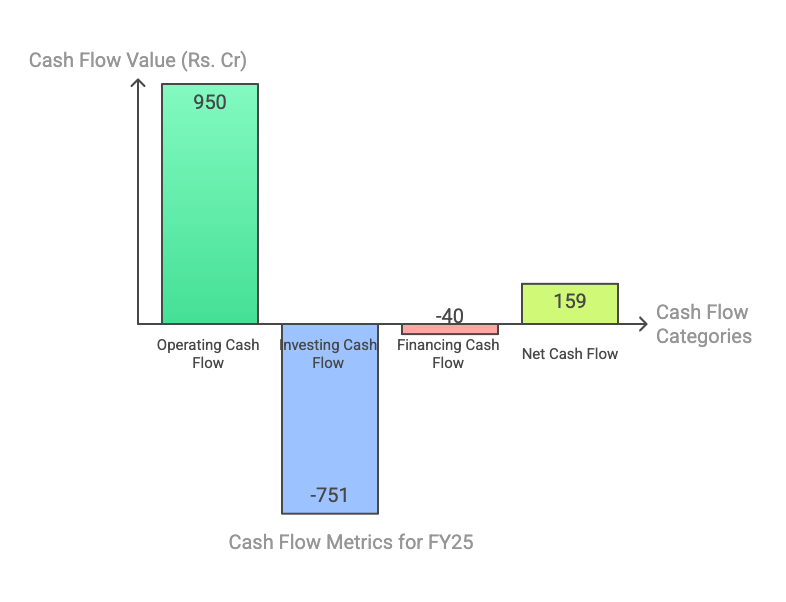

Cash Flows (FY25)

Key Insights

- Revenue and Profit Growth: MCX’s FY25 revenue grew 59.28% YoY to ₹1,113 Cr, with profit soaring 574% to ₹560 Cr, driven by increased trading volumes (Screener).

- Profitability: High ROCE (42.9%) and ROE (34.3%) reflect efficient capital utilization.

- Debt-Free Status: MCX has reduced debt significantly, enhancing financial stability.

- Valuation: A P/E ratio of 51.6 and P/B ratio of 15.4 suggest high valuation, but strong growth may justify these multiples.

Technical Analysis

Technical analysis examines stock price trends and indicators to predict future movements. Due to limitations in accessing real-time data, detailed indicators like RSI or MACD were unavailable. However, the following insights were gathered:

- Current Price: ₹5,670.50 as of May 9, 2025, down 5.57% daily (Economic Times).

- Trend: Limited data indicates a bearish signal, but MCX is less bearish than 96.54% of stocks, suggesting relative stability (TopStockResearch).

- Analyst Price Targets: Nine analysts project a 1-year price range of ₹3,400 to ₹7,800, with an average of ₹6,191.67 (TradingView).

- Performance: The stock gained 48.5% over the past year, outperforming the Nifty Financial Services index (+17.83%).

SWOT Analysis

The SWOT analysis evaluates MCX’s internal and external factors:

| Category | Details |

| Strengths | – 95.9% market share in commodity futures (FY24) – 100% share in Precious metals & stones, 99.61% in Energy, 99.80% in base metals – 7th largest globally by Commodity Futures traded – High profitability (ROCE 42.9%, ROE 34.3%) – Near debt-free status |

| Weaknesses | – High P/E (51.6) and P/B (15.4) ratios – Dependence on limited commodity segments |

| Opportunities | – Expansion into new commodity segments – Growing retail participation – Technological advancements |

| Threats | – Competition from NCDEX (3.9% market share) – SEBI regulatory changes – Commodity price volatility |

Microeconomic and Macroeconomic Factors

Microeconomic Factors

- Market Dominance: MCX’s 95.9% share in commodity futures ensures a strong competitive position (Screener).

- Operational Efficiency: Operating Profit Margin of 60% in FY25 reflects cost-effective operations.

- Shareholding Pattern: Promoters hold 21.80%, FIIs 58.10%, DIIs 19.90%, and others 0.19% (Mar 2025).

- Customer Base: 243,456 shareholders in Mar 2025 indicate growing investor interest.

Macroeconomic Factors

- Regulatory Environment: SEBI oversight ensures stability but introduces compliance risks (MCX India).

- Commodity Trends: Global supply and demand dynamics influence trading volumes.

- Economic Conditions: Inflation, GDP growth, and trade policies impact commodity prices and MCX’s performance.

Comparisons with Peers

MCX’s primary competitor is the National Commodity and Derivatives Exchange (NCDEX). A comparison is provided below:

| Metric | MCX | NCDEX |

| Market Share (FY24) | 95.9% | 3.9% |

| Revenue (FY24) | ₹778 Cr | Not available |

| Profit (FY24) | ₹148.97 Cr | Not available |

| Market Cap | ₹28,919 Cr | ~₹1,200 Cr |

• Insights: MCX’s near-monopoly dwarfs NCDEX’s market presence. While BSE and NSE are stock exchanges, MCX’s focus on commodities makes direct comparisons less relevant (Screener).

Significant Projects, Subsidiaries, Order Books, New Initiatives, Future Outlook

Subsidiaries

- Multi Commodity Exchange Clearing Corporation Ltd: Provides collateral management, risk management, and clearing and settlement services (Groww).

New Initiatives

- Gold Mini Futures: Launched trading in Gold Mini March 2025 Contract on Dec 5, 2024 (MCX India).

- MCX METLDEX®: Introduced futures trading in MCX iCOMDEX Base Metal Index for February 2025 on Nov 14, 2024 (MCX India).

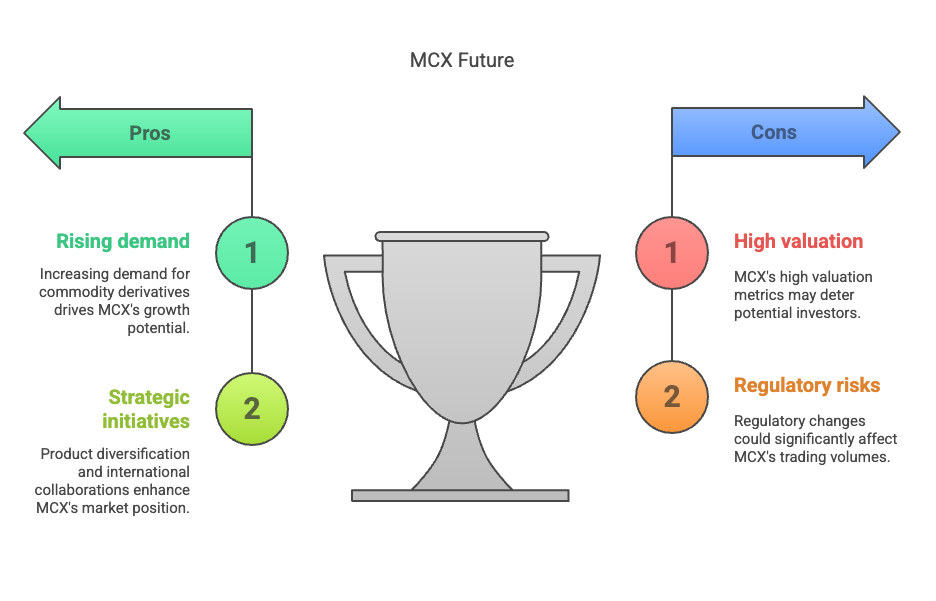

Future Outlook

- Analyst Projections: Nine analysts give a “Buy” rating with an average 1-year price target of ₹6,191.67, suggesting upside potential (TradingView).

- Growth Drivers: High revenue (23% CAGR over 5 years) and profit (25.4% CAGR) growth, coupled with market dominance, support a positive outlook.

- Strategic Focus: Expansion into new commodity segments and technological upgrades will likely enhance trading volumes.

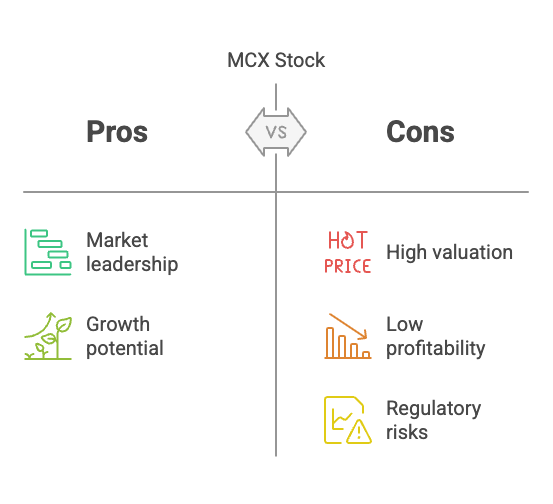

Pros and Cons

| Pros | Cons |

| Market leader with 95.9% share Strong financials with high profitability Almost debt-free Competitive dividend yield | High P/E (51.6) and P/B (15.4) ratios Dependence on commodity volatility Regulatory risks |

Conclusion: Undervalued or Overvalued?

Valuation Metrics

- P/E Ratio: 51.6, indicating potential overvaluation.

- PEG Ratio: P/E ÷ Growth Rate = 51.6 ÷ 25.4 ≈ 2.03, slightly above 2, suggesting mild overvaluation.

- P/B Ratio: 15.4, high but justifiable for a growth stock.

Analyst Consensus

- Price Target: Average of ₹6,191.67, above the current price of ₹5,670.50 (May 9, 2025).

- Rating: 7 out of 10 analysts recommend “Buy” or “Strong Buy” (Economic Times).

Growth Prospects

- MCX’s robust growth (revenue CAGR 23%, profit CAGR 25.4% over 5 years) and market leadership support its high valuation.

- New initiatives and increasing retail participation enhance future potential.

Final Assessment

While high P/E and P/B ratios suggest slight overvaluation, the analyst consensus and strong growth prospects indicate that MCX is undervalued. The current price of ₹5,670.50 is below the average analyst target of ₹6,191.67, and the “Buy” rating reflects confidence in its future performance. Investors should weigh the high valuation against MCX’s dominant market position and growth trajectory.

📢 Disclaimer

The information provided in this blog is intended solely for educational and informational purposes. It does not constitute financial advice, stock recommendations, or an offer to buy or sell any securities. Readers are advised to conduct their own research and consult with a qualified financial advisor before making any investment decisions. Please note that stock prices, financial data, and company information mentioned in this article are subject to change on trading days. For the most recent and accurate updates, kindly refer to the National Stock Exchange (NSE) and Bombay Stock Exchange (BSE) official websites.