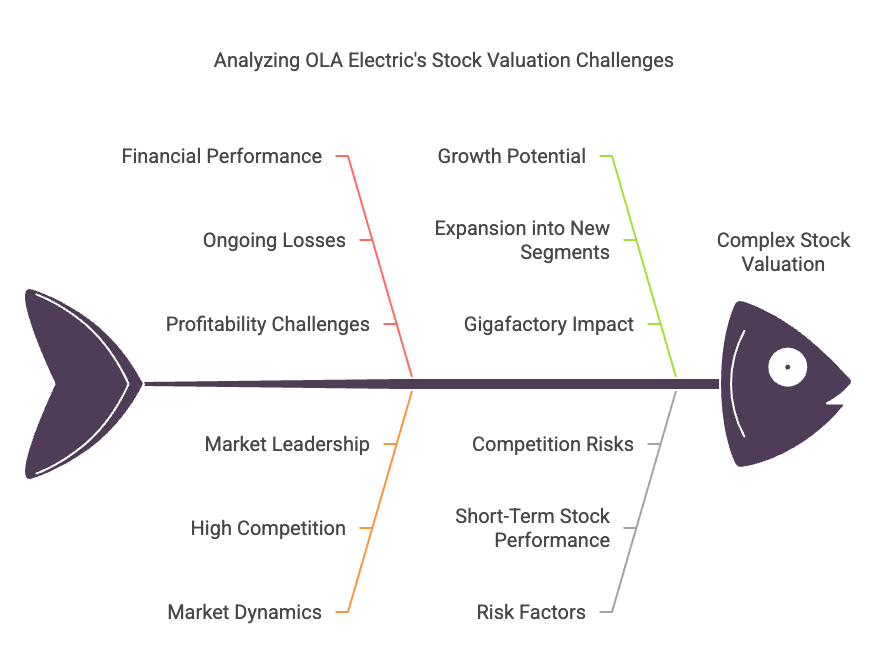

Key Points

- OLA Electric is a leading Indian EV company, but its stock valuation is complex due to ongoing losses.

- Research suggests the share is fairly valued, given growth potential and market leadership, but risks like competition exist.

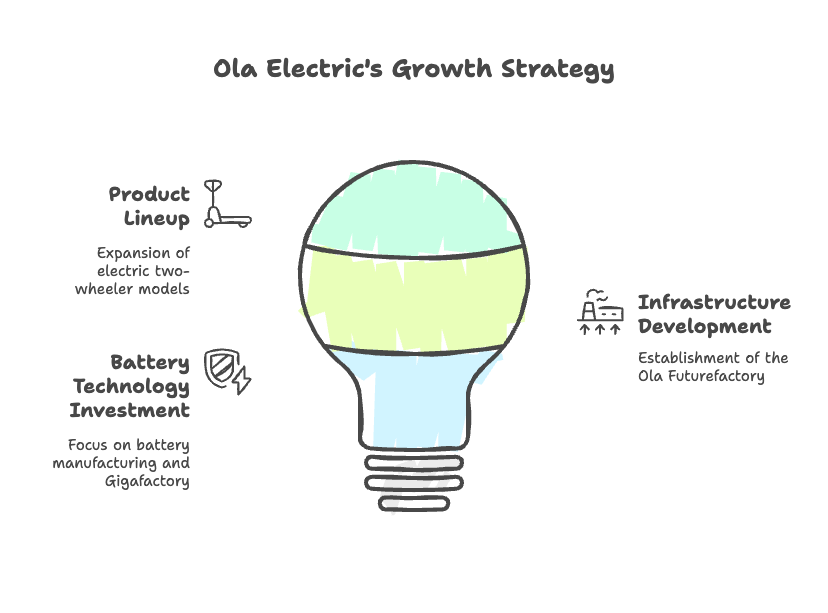

- The company is expanding into motorcycles and three-wheelers, with a new Gigafactory boosting future prospects.

- It seems likely that profitability challenges and high competition could impact short-term stock performance.

Stock Overview

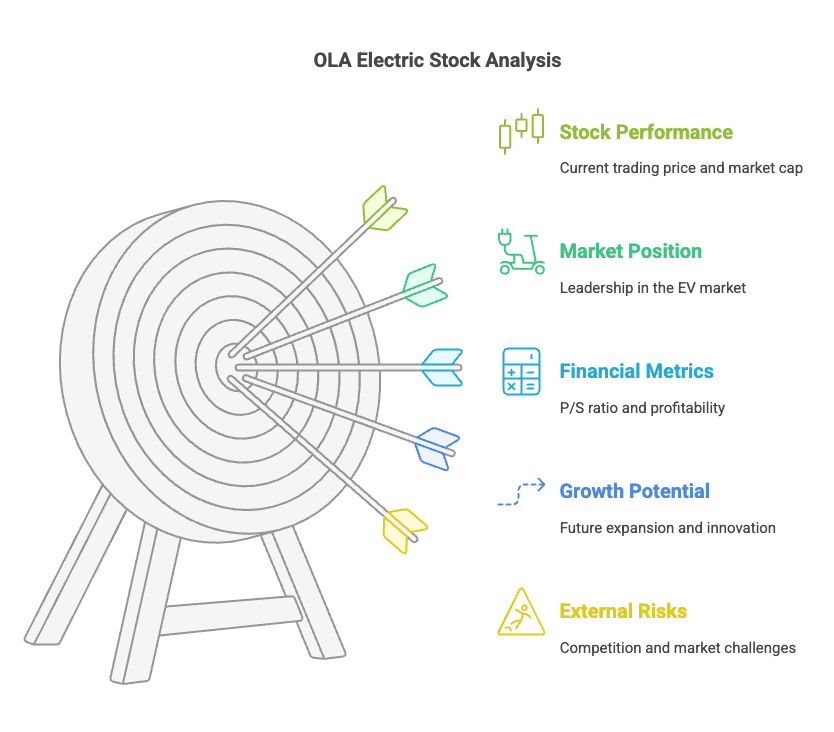

OLA Electric, a key player in India’s electric vehicle (EV) market, focuses on scooters and is expanding into new segments. Its stock, trading at ₹47.60 as of May 10, 2025, with a market cap of ₹19,876.72 Crores, is fairly valued based on its growth potential, despite current losses. The P/S ratio of 3.61 reflects its market leadership, but investors should watch for profitability and competition risks.

Financial Health

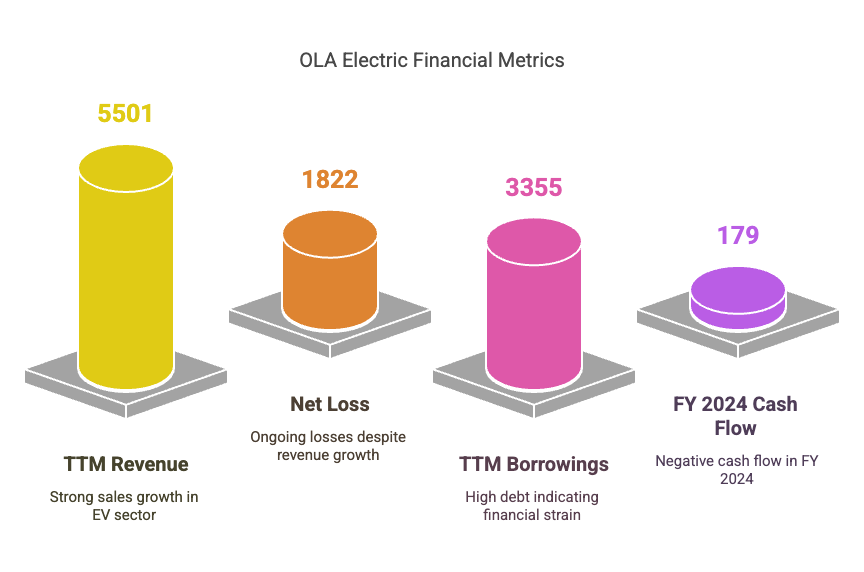

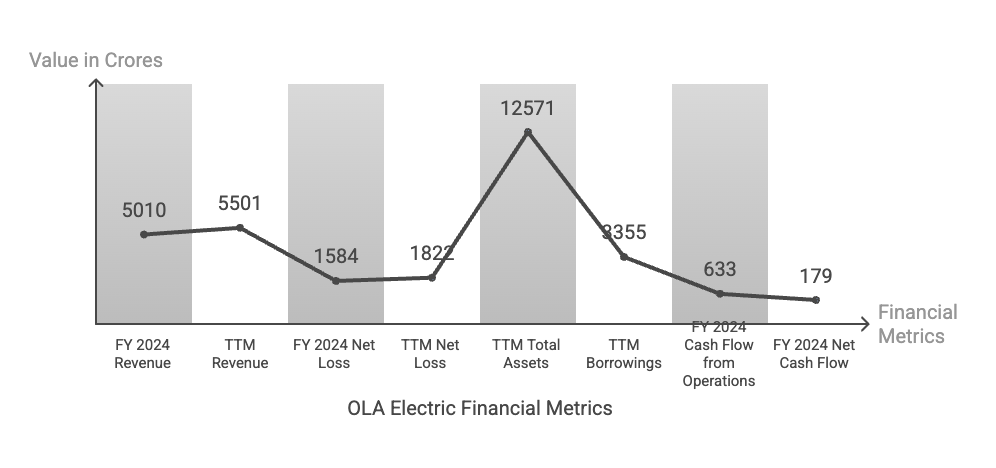

The company reported ₹5,501 Crores in TTM revenue but a net loss of ₹1,822 Crores, indicating strong sales growth but ongoing losses. High borrowings (₹3,355 Crores TTM) and negative cash flow (-₹179 Crores in FY 2024) suggest financial strain, yet its revenue growth aligns with the booming EV sector.

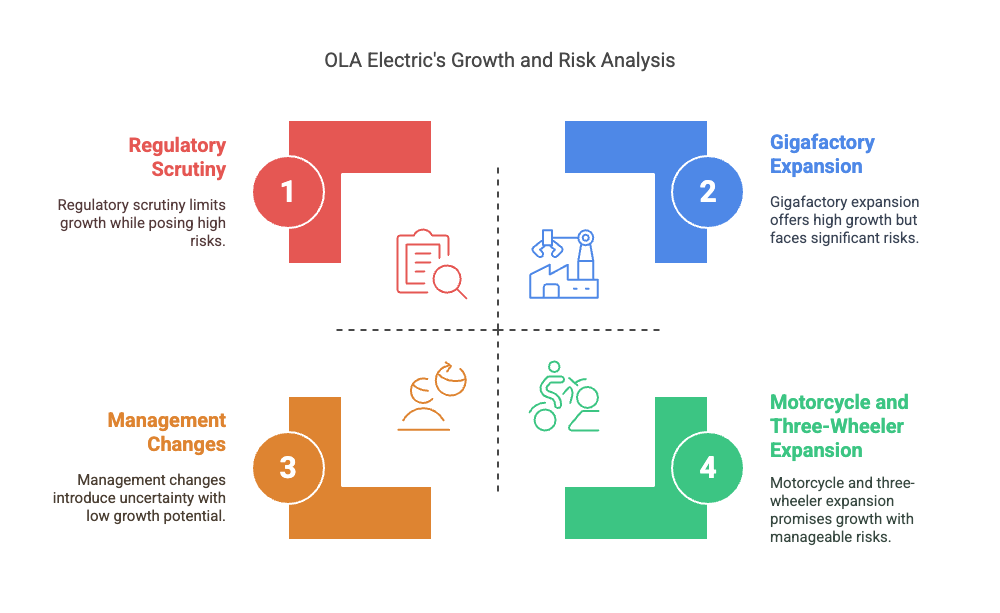

Growth and Risks

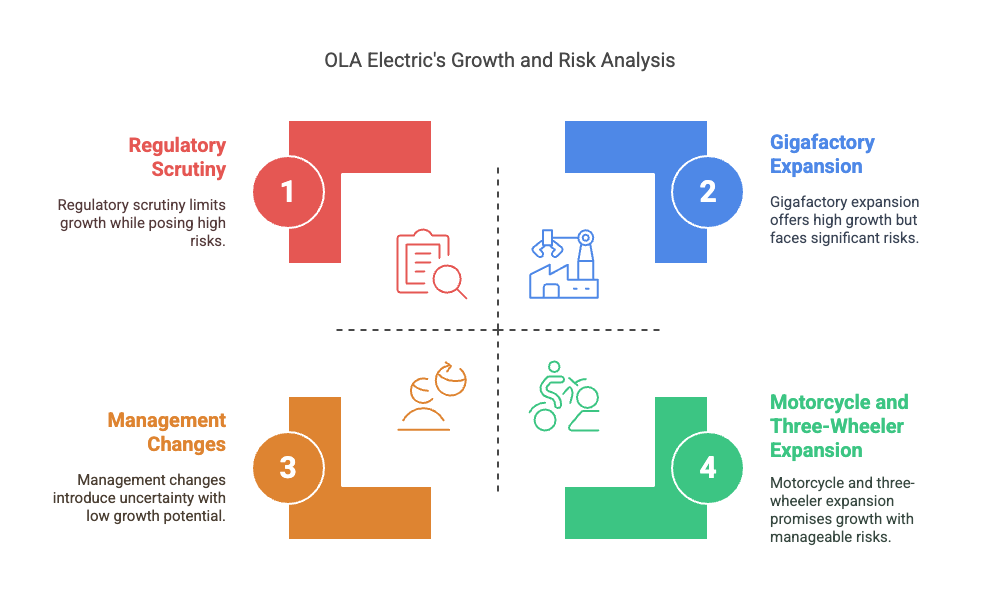

OLA Electric’s expansion into motorcycles and three-wheelers, plus a Gigafactory with 5 GWh capacity (scalable to 100 GWh), positions it for growth. However, intense competition from Ather Energy, TVS Motor, and others, along with regulatory scrutiny, poses risks. Recent management changes and layoffs add uncertainty.

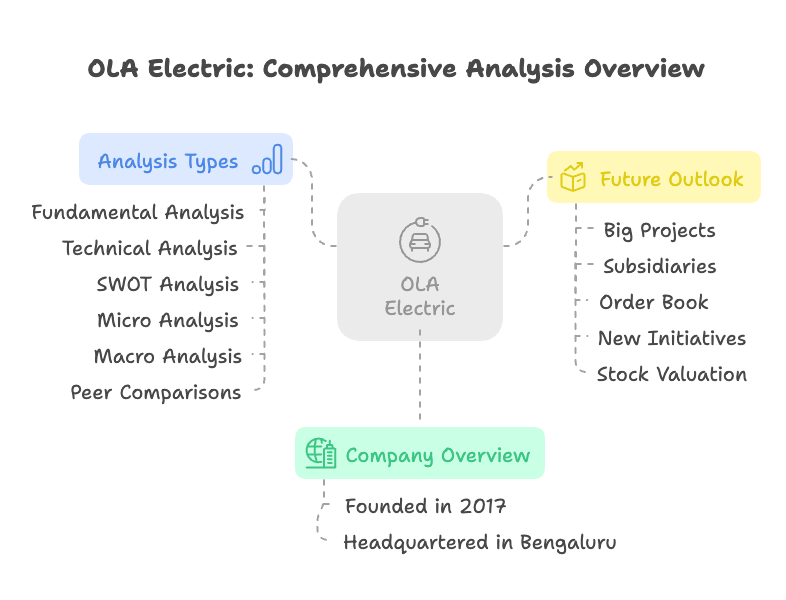

Comprehensive Analysis of Ola Electric Mobility Ltd

Introduction

OLA Electric Mobility Limited, founded in 2017 and headquartered in Bengaluru, India, is a leading manufacturer of electric vehicles, particularly electric scooters, with ambitions to expand into motorcycles and three-wheelers. This analysis covers fundamental, technical, SWOT, micro, macro, and peer comparisons, alongside details on big projects, subsidiaries, order book, new initiatives, and the future outlook of its stock, concluding with a valuation assessment as of May 10, 2025.

Fundamental Analysis

Here is a clear and concise summary of OLA Electric’s financial performance and valuation in the Indian context:

OLA Electric – Financial Overview and Valuation (As of FY 2024 & TTM)

1. Financial Performance:

- Revenue Growth:

- FY 2024 Revenue: ₹5,010 Crores

- TTM Revenue: ₹5,501 Crores

- Indicates continued top-line growth amid expanding EV adoption.

- Profitability Challenges:

- FY 2024 Net Loss: ₹1,584 Crores

- TTM Net Loss: ₹1,822 Crores

- Earnings Per Share (EPS):

- FY 2024: -₹8.10

- TTM: -₹5.98

- Reflects sustained losses driven by high R&D, manufacturing, and infrastructure costs.

- Cash Flow:

- Operating Cash Flow (FY 2024): -₹633 Crores

- Net Cash Flow (FY 2024): -₹179 Crores

- Indicates significant cash burn to support operations and expansion.

2. Balance Sheet Health:

- Total Assets (TTM): ₹12,571 Crores

- Total Borrowings: ₹3,355 Crores

- Suggests moderate to high leverage, requiring careful debt management as losses continue.

3. Valuation Metrics:

- Market Capitalization: ₹19,876.72 Crores

- Price-to-Sales (P/S) Ratio: 3.61

- Reflects investor confidence in revenue growth potential, despite losses.

- Price-to-Book (P/B) Ratio: 3.22

- Indicates stock trades at 3.22x its book value, typically high for a loss-making company.

Interpretation:

- Growth-Focused Strategy: The company is in an aggressive growth phase, prioritizing scale and innovation over near-term profitability.

- High Valuation Despite Losses: Strong investor interest and a bullish outlook on India’s EV sector may be justifying premium valuations.

- Risk Factors: Prolonged losses, high capital intensity, and market competition could pressure future cash flows and valuation if breakeven is delayed.

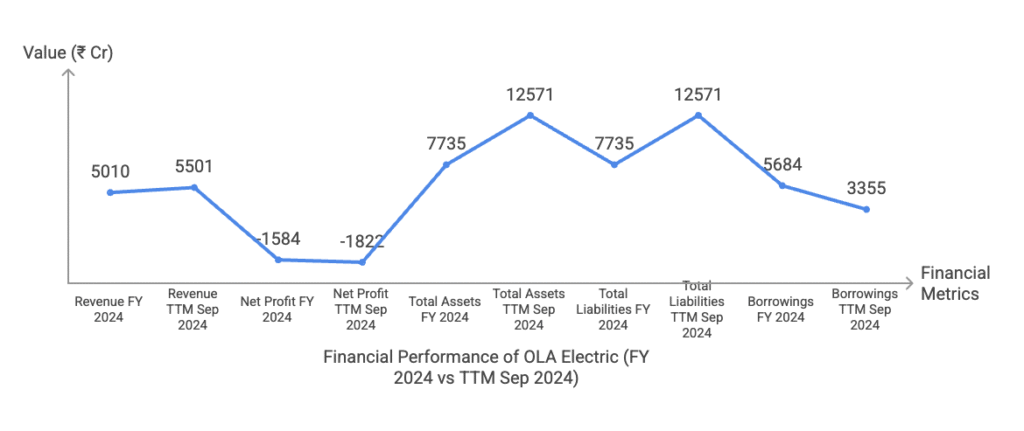

Financial Summary Table:

| Metric | FY 2024 | TTM (Sep 2024) |

| Revenue | ₹5,010 Cr | ₹5,501 Cr |

| Net Profit | -₹1,584 Cr | -₹1,822 Cr |

| EPS (Rs) | -₹8.10 | -₹5.98 |

| Total Assets | ₹7,735 Cr | ₹12,571 Cr |

| Total Liabilities | ₹7,735 Cr | ₹12,571 Cr |

| Borrowings | ₹5,684 Cr | ₹3,355 Cr |

| Cash from Operations | -₹633 Cr | N/A |

| Net Cash Flow | -₹179 Cr | N/A |

Technical Analysis

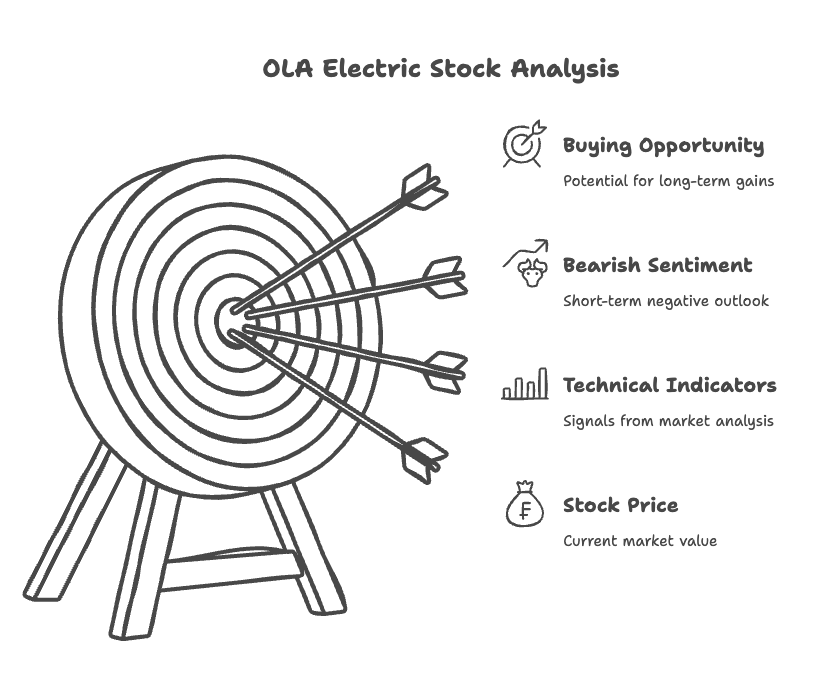

As of May 10, 2025, OLA Electric’s stock price is ₹47.60, with a 52-week high of ₹157.40 and a low of ₹45.35. Technical indicators from TradingView show an overall rating of “Strong Sell,” with oscillators and moving averages also signalling “Sell” or “Strong Sell.” This suggests short-term bearish sentiment, with the stock near its 52-week low, potentially offering a buying opportunity for long-term investors.

SWOT Analysis: Ola Electric Mobility Ltd

Strengths:

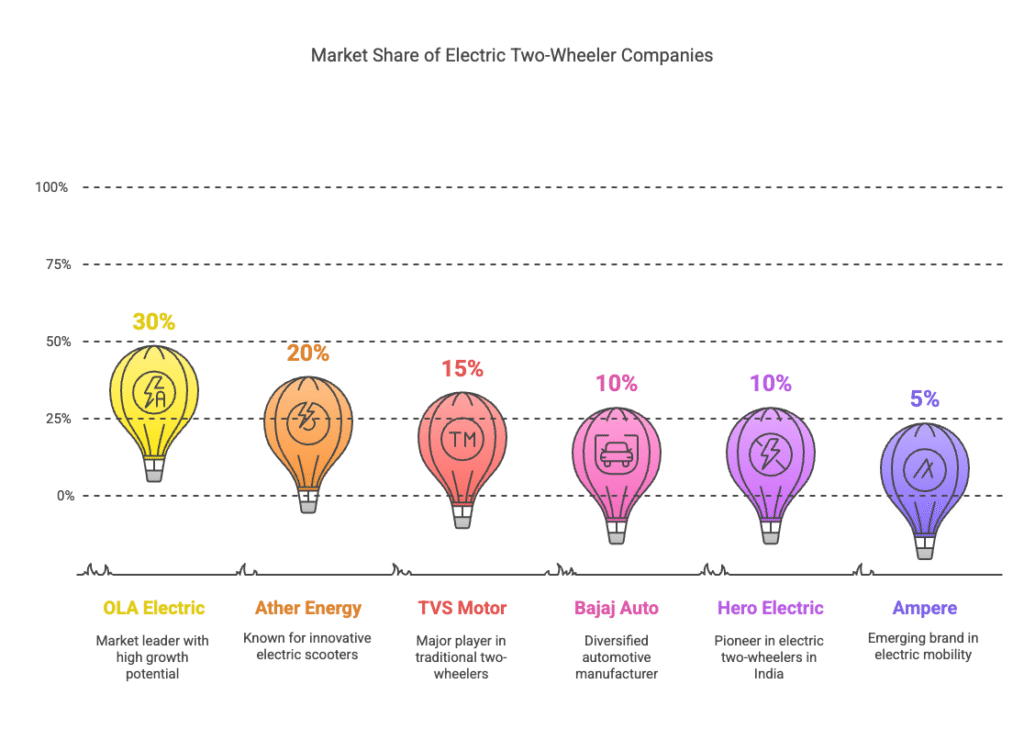

- Dominant Market Presence: Captured a 30% market share in India’s electric two-wheeler market, with over 100,000 units sold in 2023.

- Advanced Battery Technology: In-house developed batteries offer 20% higher efficiency, delivering a range of 151 km, giving it a technological edge over domestic competitors.

- Strategic Collaborations: Partnerships with Toshiba and Siemens have led to 10% cost reductions by 2024, enhancing production efficiency.

- Sustainability Leadership: Committed to carbon neutrality by 2030, with an interim goal of offsetting 1 million tons of CO₂ by 2025—aligned with India’s green transition goals.

- Massive Production Scale: Backed by a ₹2,700+ crore investment, with an annual capacity of 10 million units, positioning OLA as a manufacturing leader in India.

- Expanding Charging Network: Currently operating 1,000 charging stations, targeting 5,000 stations by 2024, improving accessibility across urban and semi-urban regions.

- High R&D Investment: Allocates 15% of revenue to R&D, fostering continued innovation in battery tech, software, and manufacturing.

Weaknesses:

- Narrow Product Line: Currently offers only two models—Ola S1 and S1 Pro—limiting choice for different customer segments (e.g., rural, budget, or performance-focused users).

- High Production Costs: Manufacturing costs of ₹80,000–₹1,00,000 lead to thin margins compared to ICE vehicles priced between ₹50,000–₹80,000.

- Heavy Reliance on Subsidies: Dependent on India’s FAME II subsidies (₹15,000 per kWh); removal or reduction could significantly affect affordability and demand.

- Supply Chain Sensitivity: Battery costs have surged by 300% since 2020, and they comprise 40% of total vehicle cost, making OLA vulnerable to material price fluctuations.

- Tier-2 and Rural Awareness Gap: Brand recognition and EV awareness in tier-2 and rural areas is low (35%) versus 70% in metro cities, limiting nationwide adoption.

- Customer Experience Issues: Satisfaction score of 60%, below the industry norm of 75–80%, citing service delays, software glitches, and inconsistent support.

- Volatile Raw Material Prices: Prices of key inputs have increased by 230% from 2020 to Q1 2023, impacting cost control.

Opportunities:

- Expanding Domestic EV Market: India’s EV two-wheeler market is rapidly growing, supported by government targets for 30% EV penetration by 2030.

- Export Potential: Demand for two-wheeler EVs in developing Asian and African markets creates export opportunities for Indian manufacturers like OLA.

- Falling Battery Costs: Projected decline in battery prices below $100 per kWh (~₹8,000) by 2025 will improve vehicle affordability and margins.

- Government Backing: Supported by India’s ₹10,000 crore FAME II scheme and ₹18,000 crore PLI scheme for advanced battery manufacturing and EV production.

- Consumer Shift to Green Mobility: Increasing environmental awareness, especially among India’s youth, with 70% of potential buyers citing sustainability as a key factor.

- Urban Transport Demand: Rising fuel prices and congestion in Indian cities are pushing demand toward electric scooters as cost-effective and eco-friendly alternatives.

Threats:

- Intensifying Local Competition: Facing strong competition from Ather Energy, TVS, Bajaj, and Hero Electric, all investing heavily in product and infrastructure development.

- Fast-Changing Technology: Innovations like solid-state batteries could make existing lithium-ion platforms obsolete, requiring constant reinvestment.

- Policy Instability: Any rollback or delay in FAME II subsidies or state-level EV incentives could negatively affect pricing and demand.

- Economic Uncertainty: Inflation (~5.5% in 2023) and potential slowdowns may affect consumer purchasing power, especially in middle and lower-income segments.

- Charging Infrastructure Gaps: While improving, many semi-urban and rural areas still lack reliable charging access, limiting EV usability and confidence.

- Consumer Hesitation: Concerns over battery life (20%), charging time (15%), and after-sales support could deter first-time EV buyers.

- Component Shortages: Dependency on imported semiconductors and battery cells continues to be a production bottleneck—highlighted by global shortages in 2021.

Micro and Macro Analysis

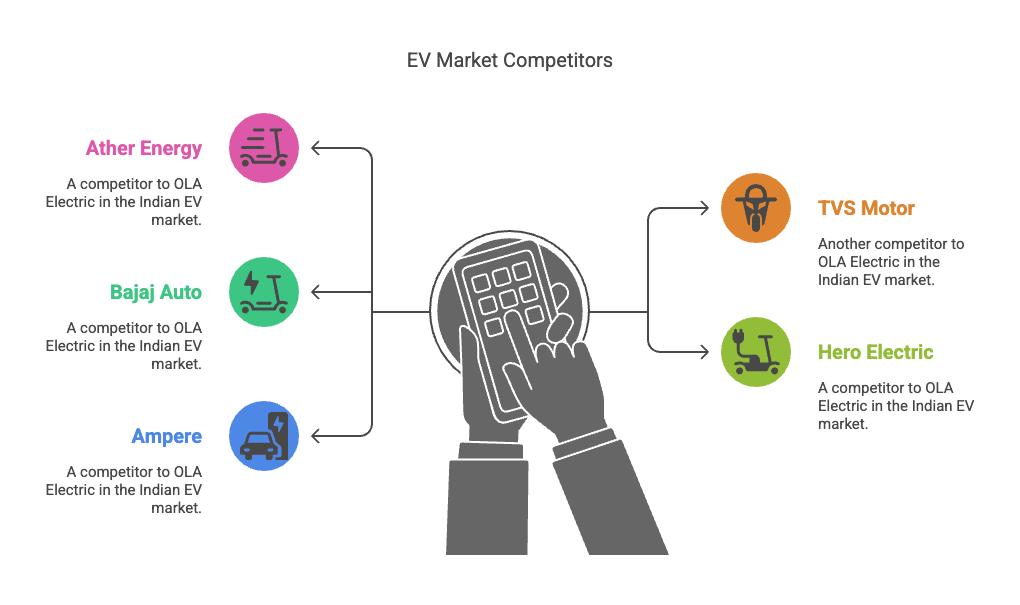

Microeconomic Factors: The Indian EV market is growing, with the two-wheeler segment at $24.87 billion by 2027 (CAGR 6.9%). OLA Electric faces competition from Ather Energy, TVS Motor, Bajaj Auto, Hero Electric, and Ampere (Greaves Electric Mobility), with high demand for affordable EVs. Supply chain challenges include battery cost volatility and import dependency.

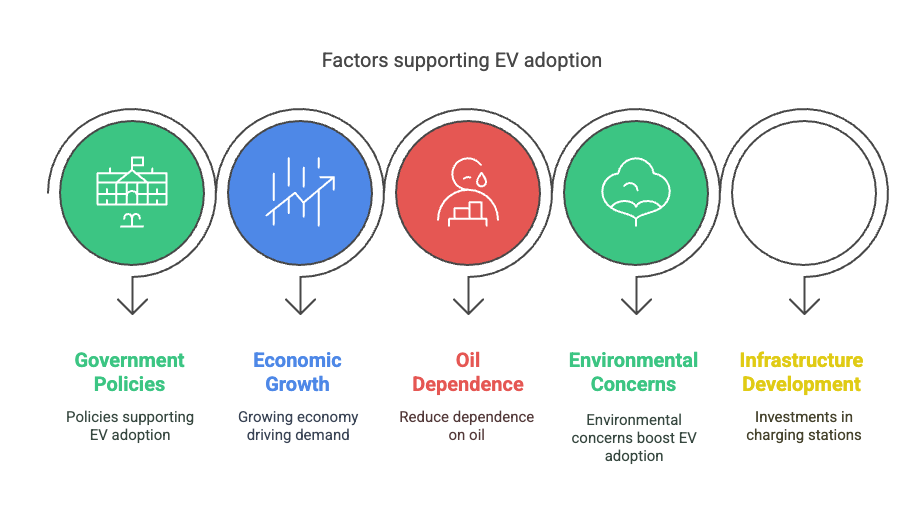

Macroeconomic Factors: Government policies like FAME II and PLI schemes support EV adoption, with India’s growing economy and urbanization driving demand. Oil dependence reduction is a priority, and environmental concerns boost EV adoption. Infrastructure development, with investments in charging stations, is crucial, aligning with government targets for renewable energy by 2030.

Peer Comparison

OLA Electric’s peers include Ather Energy, TVS Motor, Bajaj Auto, Hero Electric, and Ampere, all focusing on electric two-wheelers. While specific P/S ratios for peers are not detailed, OLA Electric’s 3.61 P/S ratio reflects its market leadership and growth potential, though it’s high for a loss-making company. Its 30% market share positions it ahead, but competition is intensifying.

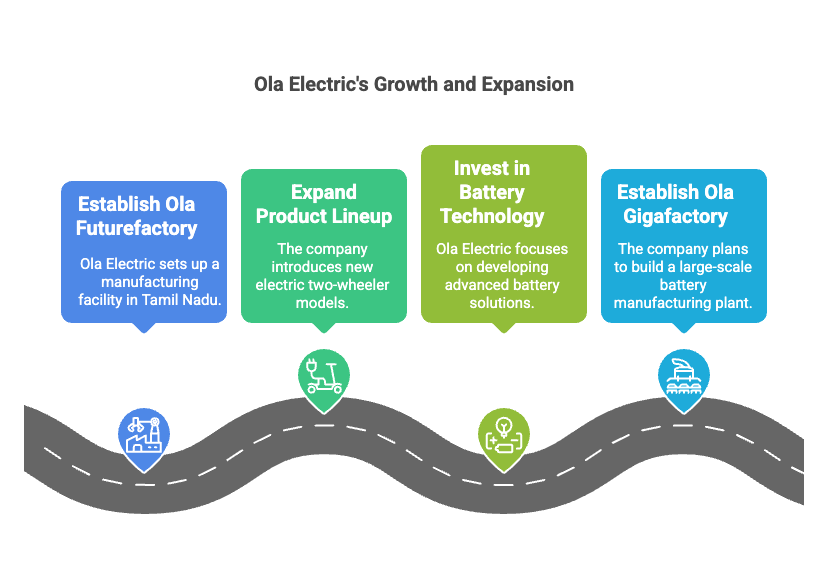

Big Projects, Subsidiaries, Order Book, and New Initiatives

- Subsidiaries: Ola Electric Technologies Private Limited (EV manufacturing) and Ola Cell Technologies Private Limited (battery cell manufacturing).

- Big Projects: The Gigafactory, India’s first lithium-ion cell facility with 5 GWh initial capacity (scalable to 100 GWh), and the Futurefactory, a 500-acre automated complex in Tamil Nadu.

- Order Book: OLA Electric has a robust reservation system for scooters, indicating a strong order pipeline, though specific numbers are not disclosed.

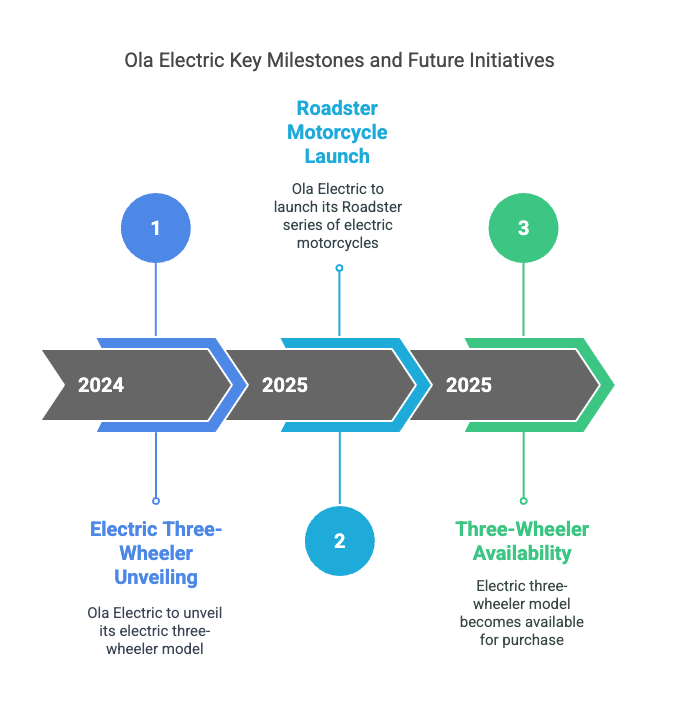

- New Initiatives: Launch of the Roadster motorcycle series in 2025, electric three-wheeler unveiling in 2024 with 2025 availability, cost-cutting measures saving ₹90 Crores monthly, and product expansion with regular launches.

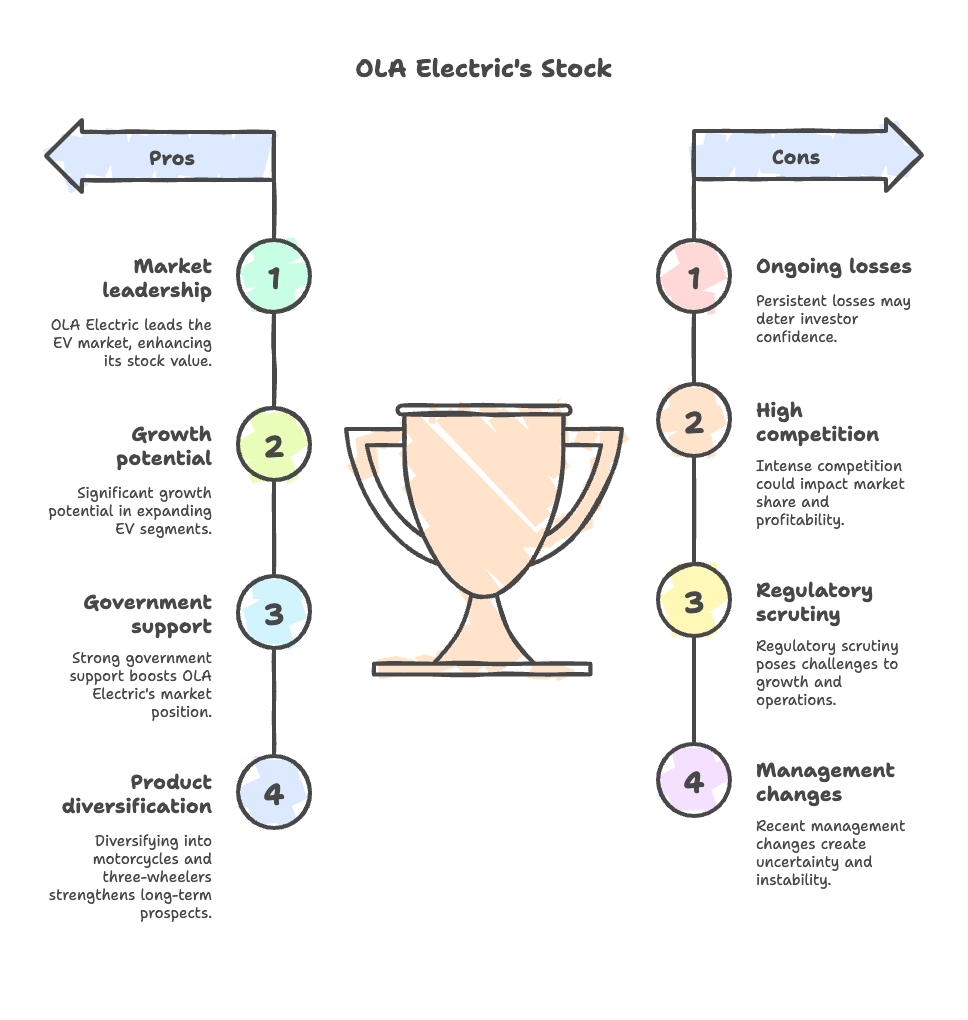

Future of the Stock

OLA Electric’s future depends on its ability to leverage growth opportunities in the EV market, with strong government support and expanding product lines. The Gigafactory and new segments like motorcycles and three-wheelers enhance long-term prospects. However, risks include ongoing losses, high competition, regulatory scrutiny, and recent management changes (e.g., resignations of CTO, CMO, and others). The stock, at ₹47.60 with a P/S ratio of 3.61, is fairly valued given its market leadership and growth potential, but investors should monitor profitability progress and execution.

Conclusion

Based on the analysis, OLA Electric’s share is fairly valued at current levels. Its market leadership, innovative initiatives, and growth in the EV sector support this, but challenges like competition and profitability need addressing. The stock’s future performance hinges on executing expansion plans and achieving financial stability.

📢 Disclaimer

The information provided in this blog is intended solely for educational and informational purposes. It does not constitute financial advice, stock recommendations, or an offer to buy or sell any securities. Readers are advised to conduct their own research and consult with a qualified financial advisor before making any investment decisions. Please note that stock prices, financial data, and company information mentioned in this article are subject to change on trading days. For the most recent and accurate updates, kindly refer to the National Stock Exchange (NSE) and Bombay Stock Exchange (BSE) official websites.