Recent Financial of Bharat Heavy Electrical Limited

| Financial Metrics (₹ Crore) | Q3 FY2024 | Q3 FY2023 | % Change |

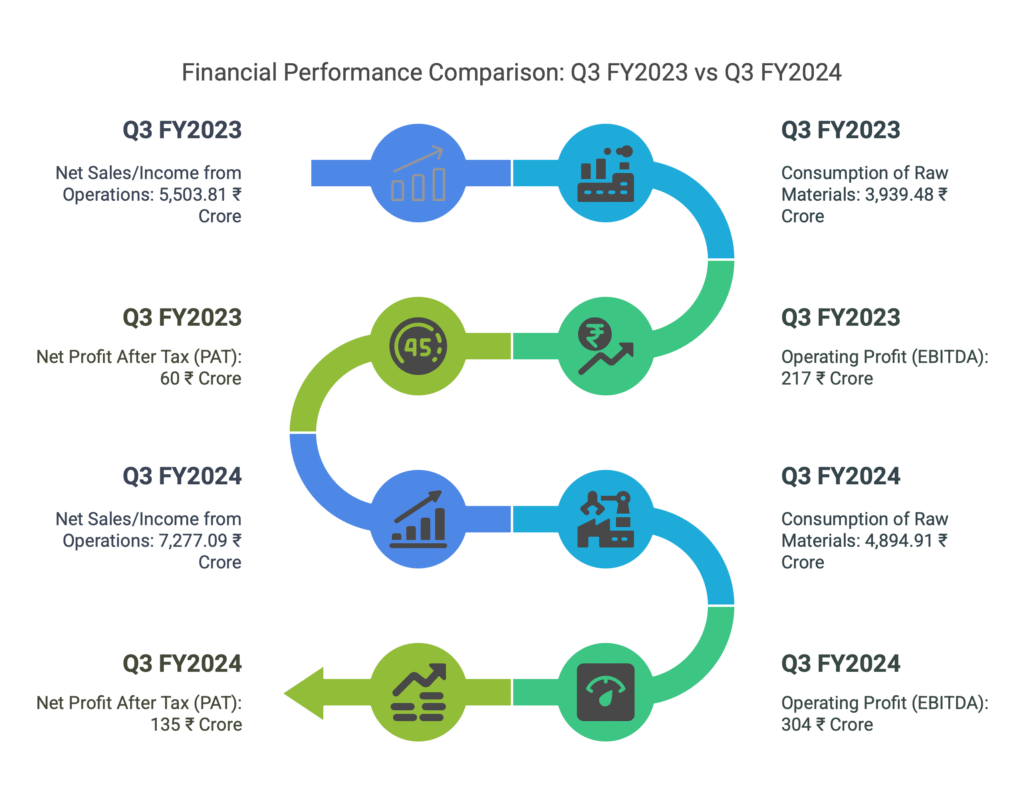

| Net Sales/Income from Operations | 7,277.09 | 5,503.81 | +32.22% |

| Consumption of Raw Materials | 4,894.91 | 3,939.48 | +24.29% |

| Operating Profit (EBITDA) | 304 | 217 | +40.09% |

| Net Profit After Tax (PAT) | 135 | 60 | +125% |

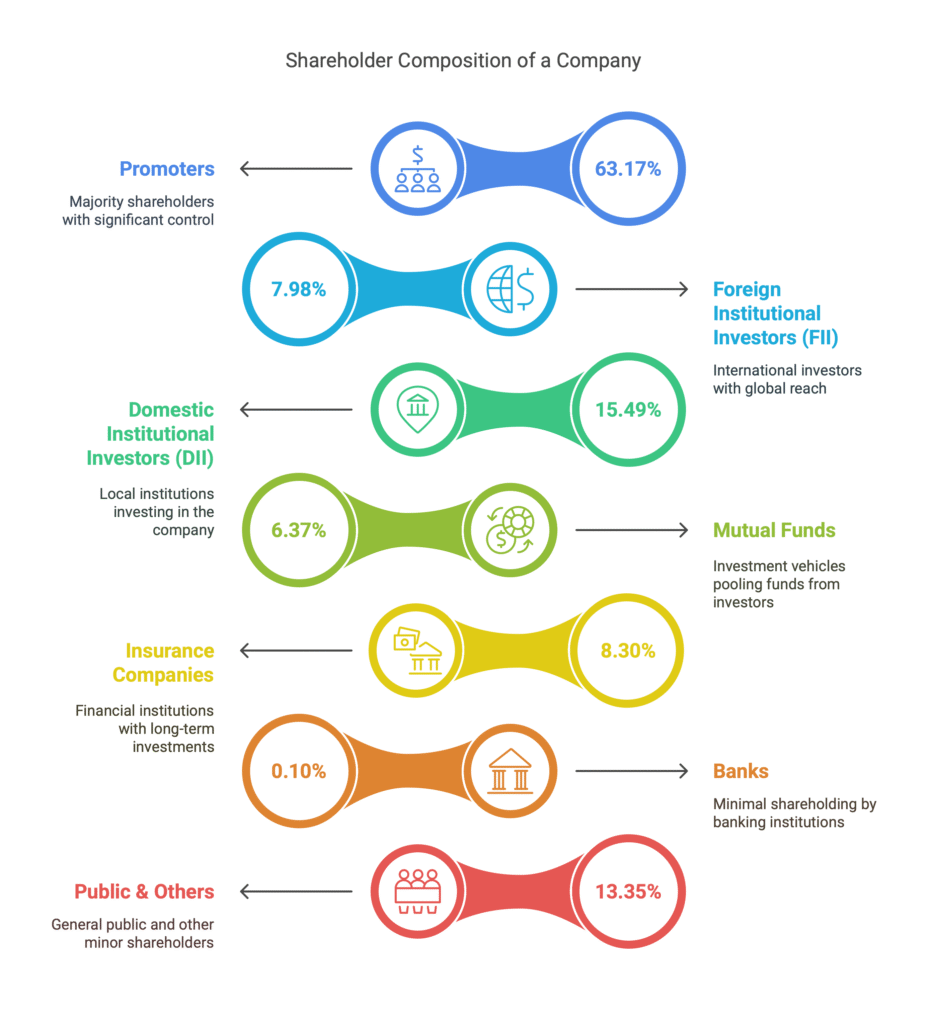

Share Holding pattern of Bharat Heavy Electrical Limited

Net Sales/Income from Operations

The net sales for Q3 FY2024 reached ₹7,277.09 crore, marking a significant increase of 32.22% from ₹5,503.81 crore in Q3 FY2023. This growth indicates a robust demand for the company’s products and services, reflecting positively on its market position.

Consumption of Raw Materials

The consumption of raw materials also saw an increase, rising to ₹4,894.91 crore in Q3 FY2024 from ₹3,939.48 crore in Q3 FY2023, which is a growth of 24.29%. This increase is consistent with the rise in production levels to meet higher sales.

Operating Profit (EBITDA)

The operating profit (EBITDA) for the quarter stood at ₹304 crore, up from ₹217 crore in the previous year, representing a substantial increase of 40.09%. This improvement in operating profit suggests enhanced operational efficiency and cost management.

Net Profit After Tax (PAT)

The net profit after tax (PAT) experienced remarkable growth, soaring to ₹135 crore in Q3 FY2024 from ₹60 crore in Q3 FY2023, which translates to an impressive increase of 125%. This significant rise in profitability underscores the company’s effective strategies and strong financial health.

why should we consider Bharat Heavy Electrical Limited

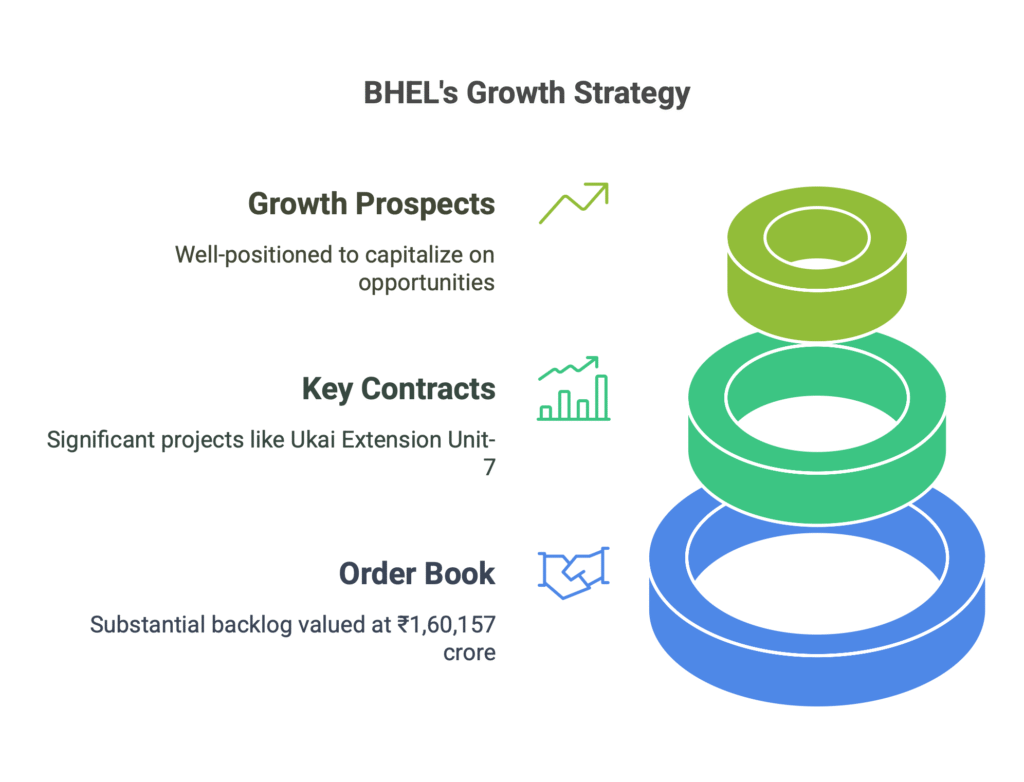

Strong order Book,

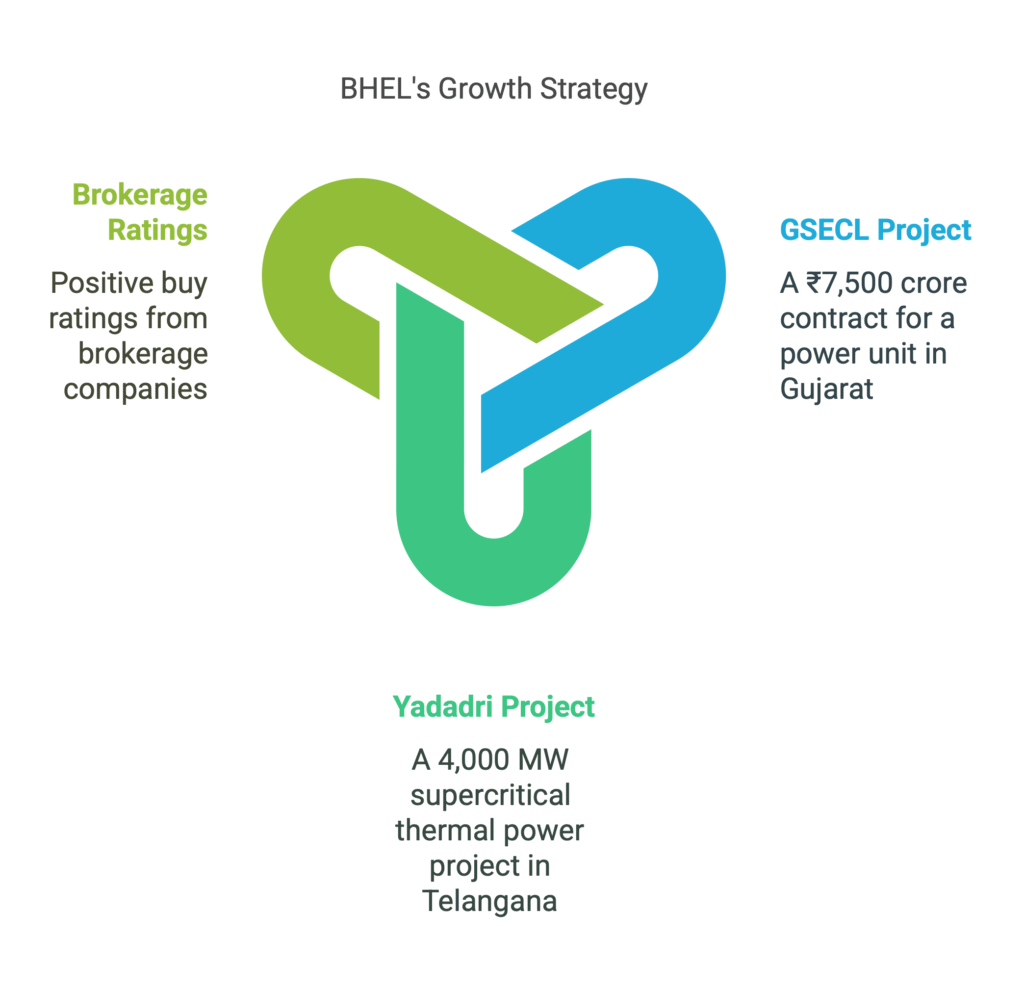

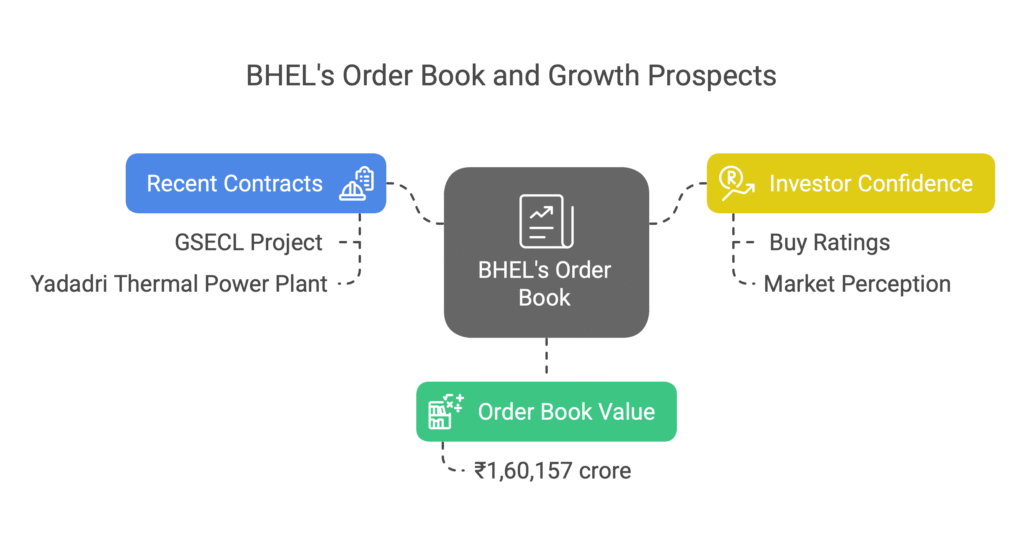

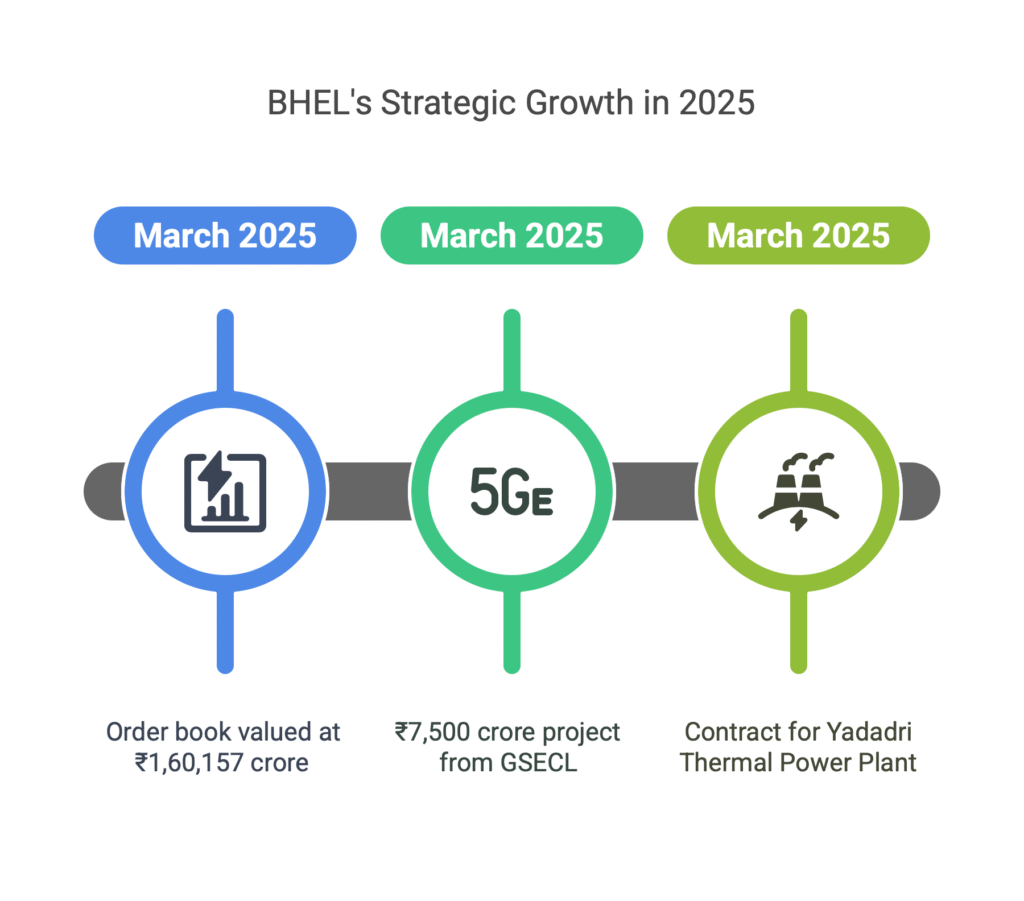

As of March 2025, Bharat Heavy Electricals Limited has an order book valued at approximately ₹1,60,157 crore. This substantial backlog includes recent contracts such as a ₹7,500 crore project from Gujarat State Electricity Corporation Limited (GSECL) for the 1×800 MW Ukai Extension Unit-7 in Tapi District, Gujarat. Additionally, BHEL secured a significant contract for the Yadadri Thermal Power Plant, a 4,000 MW supercritical thermal power project in Telangana. These orders contribute to BHEL’s robust pipeline, positioning the company for sustained growth in the power sector. Many brokerage companies have given the buy rating on it.

CONS of Bharat Heavy Electrical Limited

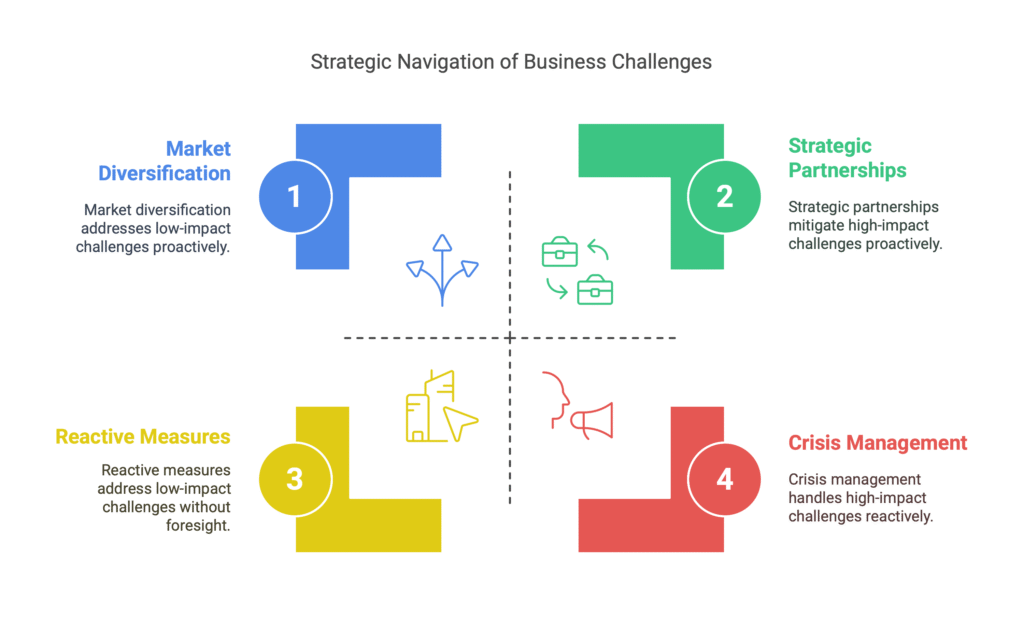

Inconsistent revenue growth.delay in government project and slow can negatively impact earnings.Decline margins dependent on government projects, limited diversification, high competitive, high competition date and working capital issue volatility in order book slow transition to renewable energy .All these issues may impact the business. various external factors can significantly impact revenue growth for businesses, particularly those reliant on government projects. Delays, declining margins, high competition, working capital issues, order book volatility, and the slow transition to renewable energy are all critical challenges that must be addressed. Companies must remain vigilant and proactive in their strategies to navigate these complexities and ensure sustainable growth in an ever-evolving market landscape.

📢 Disclaimer

This blog is for educational purposes only and is not a stock recommendation. Always consult your financial advisor and conduct your own research before making any investment decisions.